- orshu

- •

- 10 Min Read

- •

- 3 minutes ago

Key Points

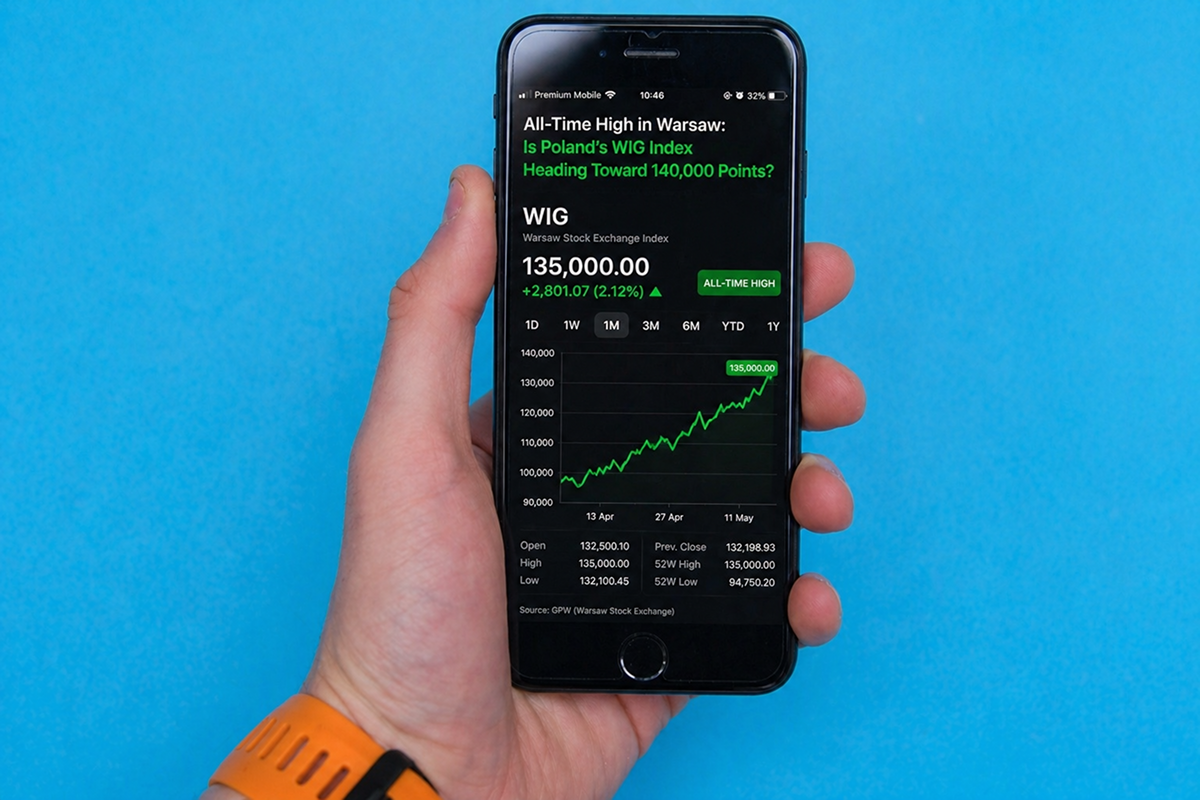

- Poland’s WIG Index is trading near record levels above 130,000 points, after gaining roughly 30% over the past year, positioning Poland as one of Europe’s standout equity markets.

- Macroeconomic stability, a policy rate of 3.75%, and strong industrial and consumer activity continue to support positive market momentum.

- Despite the bullish setup, inflation, labor-market softness, and exposure to energy-price volatility could make the path toward 140,000 points more uneven.

Poland’s equity market is emerging as one of the most compelling stories in Europe in 2026. The WIG Index, the broad benchmark of the Warsaw Stock Exchange, is trading near historic highs above 130,000 points, even after a modest decline of around 0.3% in the latest session on April 27. For a market long viewed as one of Eastern Europe’s key growth engines, this milestone signals a meaningful shift in how both domestic and foreign investors are assessing Poland’s economic trajectory.

The rally has not developed in isolation. Over the past year, the WIG Index has gained roughly 30%, and at its February 2026 peak it was up around 46% year-over-year. In global terms, that is an exceptional performance, particularly at a time when many equity markets are still navigating uncertainty around interest rates, inflation, global growth, and geopolitical risk.

Poland Is Moving From a Regional Story to a Global Investment Case

The surge in the WIG Index reflects a broader repricing of Poland’s risk profile. For years, Poland was seen as a promising European emerging market, but one that carried political, regulatory, and currency-related risks. Today, the Polish market is benefiting from a combination of relative stability, domestic growth, proximity to the European Union, and strong investment flows into industry, infrastructure, energy, and technology.

The fact that the index reached several new all-time highs over the past year, including in December, January, and February, suggests that this is not merely a short-term move driven by one strong data release. Investors appear to be pricing in a wider macroeconomic narrative: a country that continues to strengthen despite a complex global backdrop.

What Is Driving the Rally?

One of the key drivers behind the market’s advance is Poland’s industrial recovery. Industrial production has reached its highest level in three years, reinforcing the view that the country’s manufacturing base remains resilient. In an economy where industry plays a major role in growth, stronger production directly supports corporate earnings, employment demand, and investor confidence.

Private consumption is also playing a central role. Retail sales have moved close to a four-year high, supporting sectors such as banking, retail, and consumer-related equities. When households continue to spend despite inflationary pressure, it sends a strong signal about domestic economic resilience.

Another important factor is the improvement in Poland’s relationship with the European Union. Greater political stability and stronger access to European funding for infrastructure, energy, and regional development projects have improved market sentiment. For institutional investors, a stronger connection to the EU helps reduce Poland’s risk premium and increases its appeal relative to other emerging markets.

Interest Rates Are Stable, but Inflation Is Back in Focus

One of the most important variables for the market’s next move is monetary policy. Poland’s benchmark interest rate has remained stable at 3.75%, giving companies a relatively manageable financing environment. For equity markets, this matters. A stable rate environment supports company valuations, especially in capital-intensive sectors such as industry, infrastructure, and technology.

However, inflation has risen to 3%, up from 2.1%, reaching its highest level in eight months. This is the key risk investors need to monitor. If inflation continues to accelerate, Poland’s central bank may be forced to adopt a more hawkish stance. That would raise borrowing costs, weigh on risk appetite, and pressure growth-oriented sectors.

In other words, the current setup remains constructive: solid growth, stable interest rates, and strong investor confidence. But if inflation begins to erode that balance, the market’s optimistic pricing could face a serious test.

The Risks Are Not Only Domestic

Poland’s market is also exposed to external risks, particularly through energy prices. As an industrial economy, Poland is highly sensitive to volatility in oil and gas prices. Uncertainty around the Strait of Hormuz and broader Middle East tensions could feed into higher energy costs, affecting production expenses, corporate margins, and consumer prices.

The labor market also presents a more mixed picture. The unemployment rate remains stable at around 6.1%, but employment data has declined more than expected. That is an important warning sign. If labor-market softness deepens, it could eventually affect household spending, which has been one of the main pillars behind Poland’s recent market strength.

Is 140,000 Points a Realistic Target?

The central question now is whether the WIG Index can move toward 140,000 points by the end of the year. From both a technical and psychological perspective, the 130,000-point level has become a key test. As long as the index holds above that area, investors are likely to view short-term declines as healthy profit-taking rather than the beginning of a broader trend reversal.

The index’s gain of roughly 7.6% over the past month also suggests that momentum remains positive. Still, the closer the market gets to new highs, the higher the expectations become. At this stage, investors will not be satisfied with simply “good” data. They will need to see continued improvement, stable monetary policy, and resilient consumer demand to justify current valuations.

The sectors that could lead the next phase of gains include green energy, advanced manufacturing, and technology, particularly companies benefiting from the adoption of artificial intelligence in industrial processes and business services. At the same time, banks and retailers will remain important indicators of the health of the domestic economy.

Comparison, examination, and analysis between investment houses

Leave your details, and an expert from our team will get back to you as soon as possible

* This article, in whole or in part, does not contain any promise of investment returns, nor does it constitute professional advice to make investments in any particular field.

To read more about the full disclaimer, click here

- orshu

- •

- 4 Min Read

- •

- ago 19 minutes

SKN | European Markets Mixed as Modest Gains in Germany Offset Broader Weakness

European markets delivered a mixed session on Monday, April 27, 2026, as modest gains in select indices were offset by

- ago 19 minutes

- •

- 4 Min Read

European markets delivered a mixed session on Monday, April 27, 2026, as modest gains in select indices were offset by

- orshu

- •

- 6 Min Read

- •

- ago 4 days

SKN | The S&P 500 Just Broke the “Fear Index”: Is a 5-Year Double on the Horizon?

While global headlines remain fixated on military tensions with Iran and the closure of the Strait of Hormuz, Wall Street

- ago 4 days

- •

- 6 Min Read

While global headlines remain fixated on military tensions with Iran and the closure of the Strait of Hormuz, Wall Street

- orshu

- •

- 5 Min Read

- •

- ago 4 days

SKN | Asia Markets Close Mostly Lower on April 23, 2026 as Korea Extends Gains While Regional Weakness Broadens

Asian markets closed April 23, 2026, mostly lower, as regional weakness broadened despite continued strength in South Korea. The session

- ago 4 days

- •

- 5 Min Read

Asian markets closed April 23, 2026, mostly lower, as regional weakness broadened despite continued strength in South Korea. The session

- orshu

- •

- 4 Min Read

- •

- ago 4 days

SKN | European Markets Slip as Broad Weakness Offsets Gains in France

European markets moved lower on Thursday, April 23, 2026, as broad-based weakness weighed on regional equities despite isolated strength in

- ago 4 days

- •

- 4 Min Read

European markets moved lower on Thursday, April 23, 2026, as broad-based weakness weighed on regional equities despite isolated strength in