- sagi habasov

- •

- 7 Min Read

- •

- 1 week ago

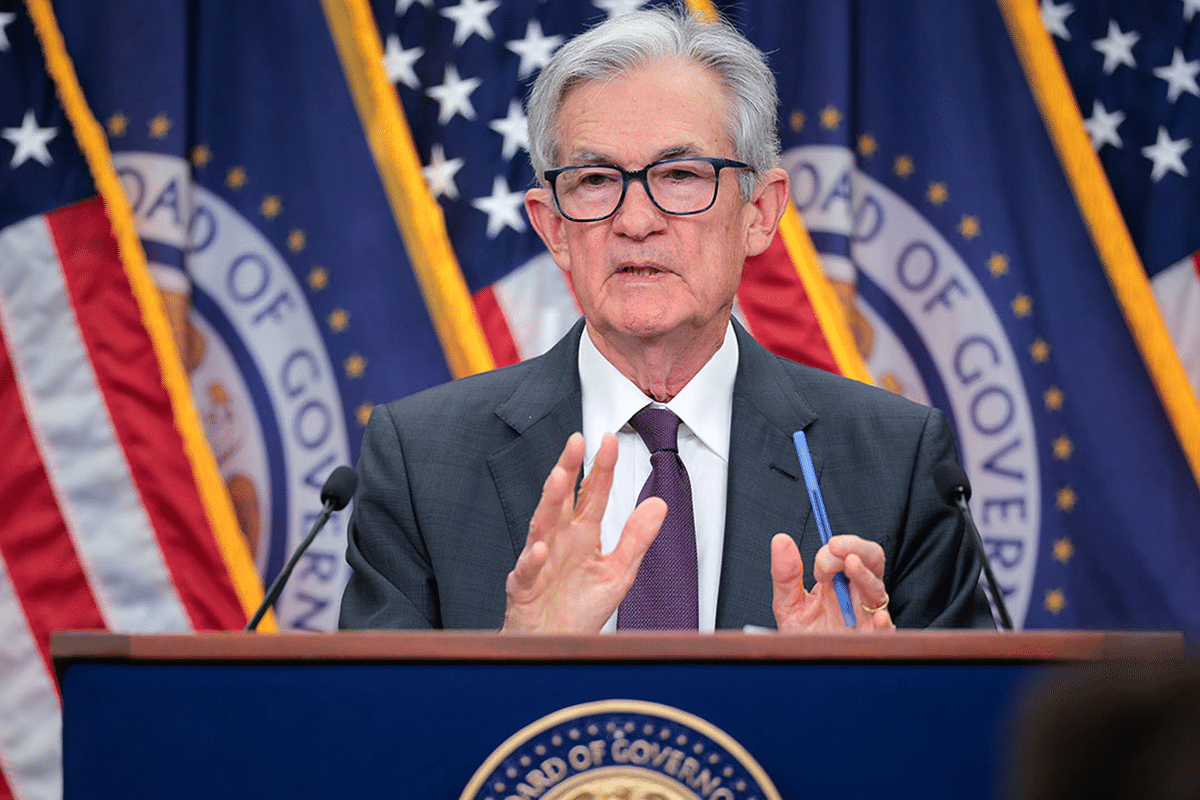

Key Points

- Treasury yields edged higher ahead of the Fed’s January meeting minutes, reflecting cautious positioning.

- The Fed held rates steady at 3.5%–3.75%, with investors seeking insight into internal hawk-dove dynamics.

- Friday’s PCE inflation data could shape expectations for the timing and scale of future rate cuts.

U.S. Treasury yields ticked higher as investors positioned cautiously ahead of the Federal Reserve’s January meeting minutes, due for release at 2 p.m. ET. The modest move in yields reflects a market in wait-and-see mode, with traders seeking clearer guidance on the central bank’s reaction function after it opted to hold rates steady for the first time since restarting policy normalization in September 2025.

The bond market’s subtle adjustment underscores how sensitive fixed-income investors remain to any hint of policy recalibration in a year already marked by volatile rate expectations.

Rates on Hold, But For How Long?

At its January meeting, the Federal Open Market Committee left the benchmark interest rate unchanged at a range of 3.5% to 3.75%, in line with market expectations. Fed Chair Jerome Powell reiterated that decisions would be made “meeting by meeting,” guided strictly by incoming economic data.

That language signaled flexibility but offered little forward clarity, leaving investors to dissect every nuance in subsequent commentary. For bond markets, where valuations hinge on the anticipated trajectory of short-term rates, even minor rhetorical shifts can trigger meaningful repricing.

Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, noted that market participants will closely examine the dynamic between hawkish and dovish members of the committee. The January pause marked the first hold since the Fed resumed tightening efforts late last year, making the tone of internal debate particularly significant.

Understanding the Fed’s Reaction Function

Beyond headline decisions, investors are focused on the Fed’s “reaction function” — how policymakers interpret and respond to evolving data. The minutes may reveal the underlying rationale for refraining from a rate cut in January, especially as inflation has shown signs of moderation.

If the minutes suggest broad concern over persistent inflationary pressures, yields could extend their recent gains. Conversely, signs that several officials were leaning toward easing — but opted for patience — may reinforce expectations of cuts later this year.

This delicate balance has created a tug-of-war in the bond market. Money markets have fluctuated between pricing in multiple cuts in 2026 and scaling back expectations amid resilient economic data. The Treasury market’s slight upward drift in yields suggests investors are hedging against the possibility that the Fed maintains restrictive policy longer than previously assumed.

PCE Data Could Be the Next Catalyst

Attention will quickly shift to Friday’s release of the personal consumption expenditures (PCE) price index, the Fed’s preferred inflation measure. The data could either validate the central bank’s cautious stance or reignite debate over the urgency of policy easing.

For equity markets, bond yields remain a critical variable. Higher yields tend to pressure growth stocks by raising discount rates, while lower yields typically support risk appetite. As a result, the interplay between Fed communication and economic data continues to ripple across asset classes, from Treasuries to equities and foreign exchange.

In the near term, volatility may remain contained until clearer signals emerge. But the bond market’s incremental move higher ahead of the minutes highlights a broader theme: investors are no longer betting aggressively on rapid rate cuts, and the burden of proof now lies with incoming data.

Comparison, examination, and analysis between investment houses

Leave your details, and an expert from our team will get back to you as soon as possible

* This article, in whole or in part, does not contain any promise of investment returns, nor does it constitute professional advice to make investments in any particular field.

To read more about the full disclaimer, click here

- omer bar

- •

- 6 Min Read

- •

- ago 3 days

SKN | Dollar Rebounds Above 97.8: Is Tariff Turbulence Reviving Safe-Haven Demand?

The U.S. dollar regained ground Tuesday, with the Dollar Index climbing above 97.8 after weakness in the prior session, as

- ago 3 days

- •

- 6 Min Read

The U.S. dollar regained ground Tuesday, with the Dollar Index climbing above 97.8 after weakness in the prior session, as

- omer bar

- •

- 7 Min Read

- •

- ago 4 days

SKN | Are Treasury Bears Regaining Control as Deficit Risks and Fed Signals Shift Bond Momentum?

Momentum in the $31 trillion US Treasury market is tilting back toward bond bears as a combination of fiscal uncertainty,

- ago 4 days

- •

- 7 Min Read

Momentum in the $31 trillion US Treasury market is tilting back toward bond bears as a combination of fiscal uncertainty,

- sagi habasov

- •

- 6 Min Read

- •

- ago 1 week

SKN | Stocks and Bonds Drift in Holiday-Thinned Trade: What the Muted Volatility Signals for Global Investors

Stocks and bonds moved within narrow but uneven ranges as holiday-thinned trading reduced liquidity across major financial centers. With

- ago 1 week

- •

- 6 Min Read

Stocks and bonds moved within narrow but uneven ranges as holiday-thinned trading reduced liquidity across major financial centers. With

- Ronny Mor

- •

- 6 Min Read

- •

- ago 2 weeks

SKN | Carry Trade and Commodities Shield EM Currencies: Are They Now More Stable Than G-7 FX?

Emerging-market currencies are showing an unusual degree of resilience relative to their developed-market peers, challenging long-standing assumptions about foreign-exchange

- ago 2 weeks

- •

- 6 Min Read

Emerging-market currencies are showing an unusual degree of resilience relative to their developed-market peers, challenging long-standing assumptions about foreign-exchange